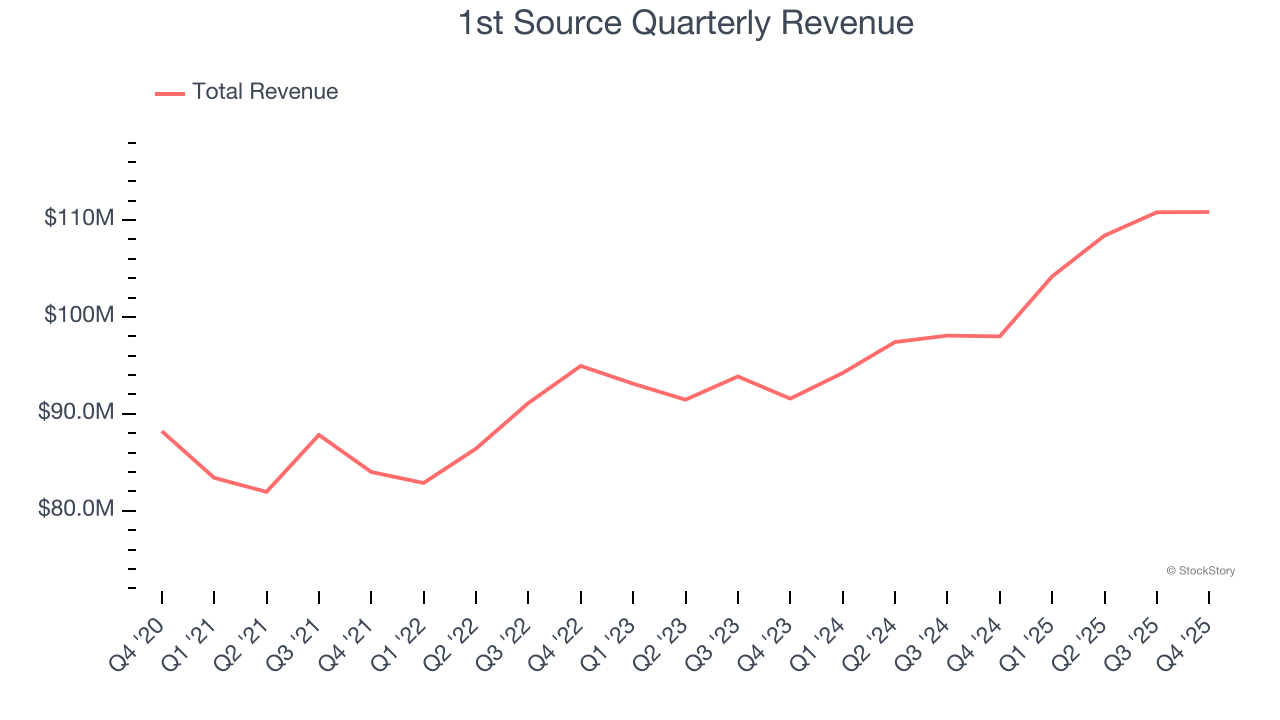

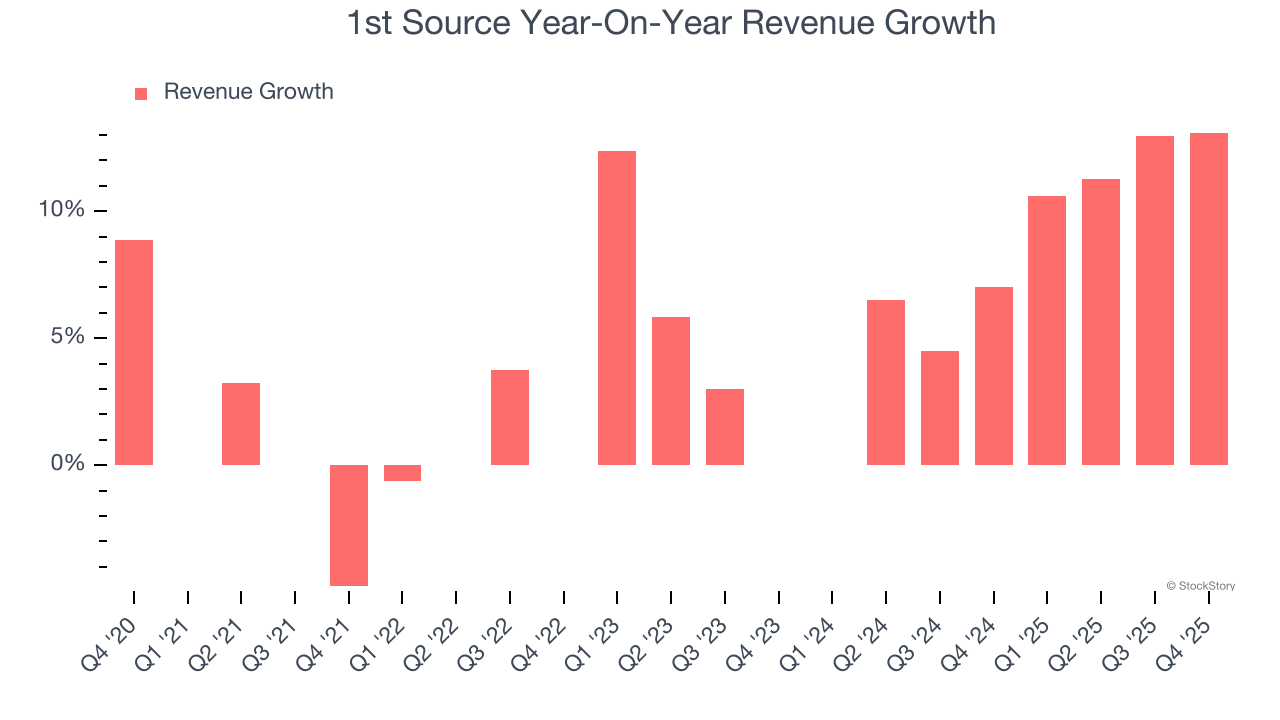

Regional banking company 1st Source (NASDAQ:SRCE) met Wall Streets revenue expectations in Q4 CY2025, with sales up 13.1% year on year to $110.8 million. Its non-GAAP profit of $1.87 per share was 16.1% above analysts’ consensus estimates.

Is now the time to buy 1st Source? Find out by accessing our full research report, it’s free.

1st Source (SRCE) Q4 CY2025 Highlights:

- Net Interest Income: $93.3 million vs analyst estimates of $87.46 million (17.6% year-on-year growth, 6.7% beat)

- Net Interest Margin: 4.3% vs analyst estimates of 4% (25.3 basis point beat)

- Revenue: $110.8 million vs analyst estimates of $111 million (13.1% year-on-year growth, in line)

- Efficiency Ratio: 51% vs analyst estimates of 49.2% (186.3 basis point miss)

- Adjusted EPS: $1.87 vs analyst estimates of $1.61 (16.1% beat)

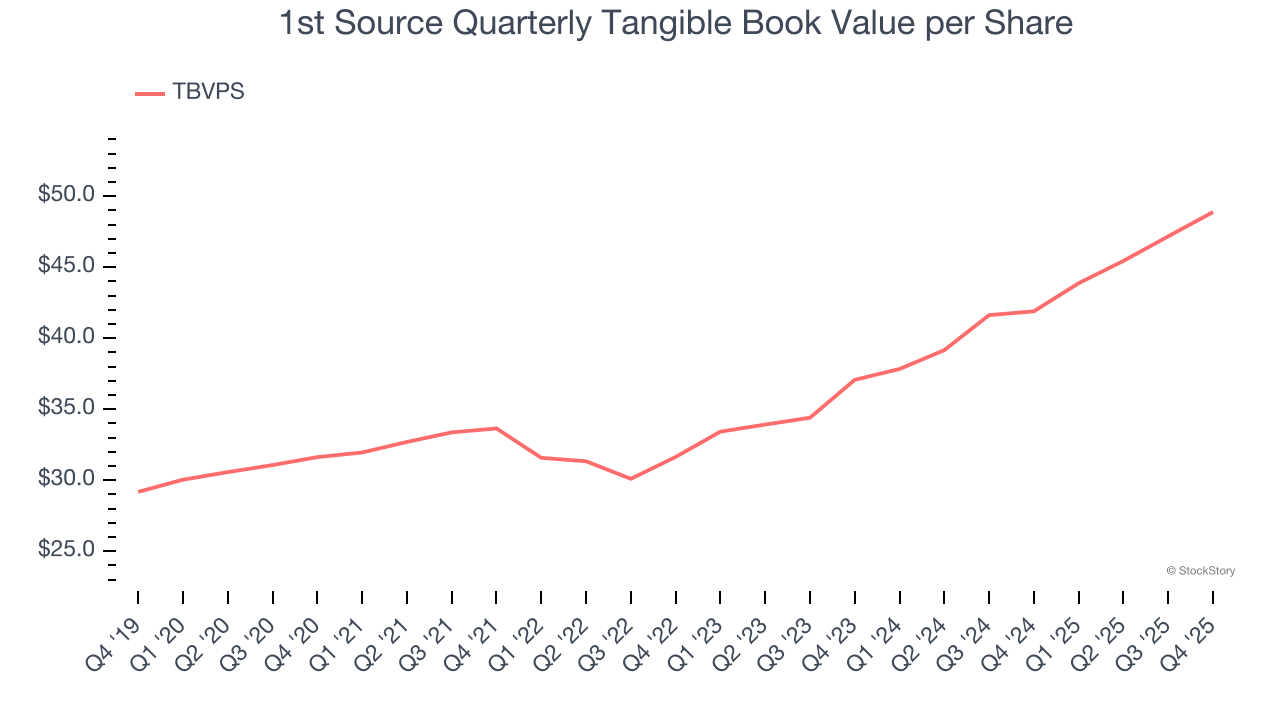

- Tangible Book Value per Share: $48.88 vs analyst estimates of $49.10 (16.7% year-on-year growth, in line)

- Market Capitalization: $1.65 billion

Andrea G. Short, President and Chief Executive Officer, commented, "We are pleased to announce record net income for the fifth year in a row and we reached our 38th consecutive year of dividend growth. We were able to grow average loans and leases by $336.29 million or 5.10% and average deposits, net of brokered deposits, increased by $338.84 million or 5.18% from 2024. Higher rates on investment securities, relatively stable rates on loans and leases, and lower deposit and short-term borrowing rates resulted in tax-equivalent net interest margin expansion during 2025 to 4.07% from 3.64% in 2024. During the fourth quarter, we also experienced margin expansion of 20 basis points. Net interest recoveries had a positive 14 basis point impact on the fourth quarter 2025 tax-equivalent net interest margin compared to a positive three basis point impact during the previous quarter. We had net charge-offs to average loans and leases of 0.06% in 2025 compared to 0.09% in 2024. These positive income statement results were supported by a strong balance sheet. During the year, we maintained strong liquidity and upheld our historically conservative capital structure. I am extremely proud that my colleagues were able to achieve such positive results despite the unique challenges of the last several years.

Company Overview

Tracing its roots back to 1863 during the Civil War era, 1st Source Corporation (NASDAQ:SRCE) is a regional bank holding company that provides commercial, consumer, specialty finance, and wealth management services across Indiana, Michigan, and Florida.

Sales Growth

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Over the last five years, 1st Source grew its revenue at a sluggish 5.6% compounded annual growth rate. This wasn’t a great result compared to the rest of the banking sector, but there are still things to like about 1st Source.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. 1st Source’s annualized revenue growth of 8.3% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, 1st Source’s year-on-year revenue growth was 13.1%, and its $110.8 million of revenue was in line with Wall Street’s estimates.

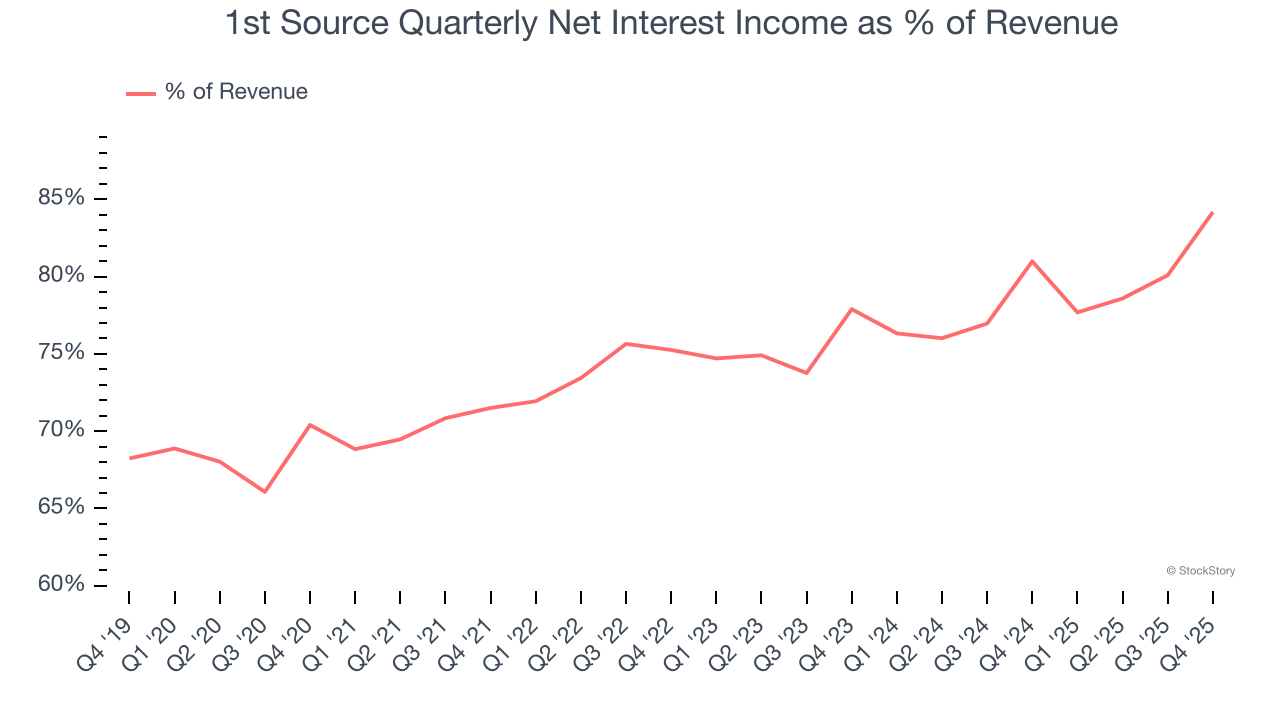

Net interest income made up 75.5% of the company’s total revenue during the last five years, meaning lending operations are 1st Source’s largest source of revenue.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

1st Source’s TBVPS grew at an exceptional 9.1% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 14.8% annually over the last two years from $37.06 to $48.88 per share.

Over the next 12 months, Consensus estimates call for 1st Source’s TBVPS to grow by 10.1% to $53.81, mediocre growth rate.

Key Takeaways from 1st Source’s Q4 Results

We were impressed by how significantly 1st Source blew past analysts’ net interest income expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $66.33 immediately after reporting.

1st Source had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).